Published by Bruce McNevin on Feb 27, 2023 8:46:19 PM

Three months ago, there was widespread speculation from many commentators that the US economy was in a recession. At that time, our analysis derived from typical NBER recession indicators showed that there was a very low probability that the economy was in recession. The picture today suggests that the US economy is even farther away from recession than it was three months ago.

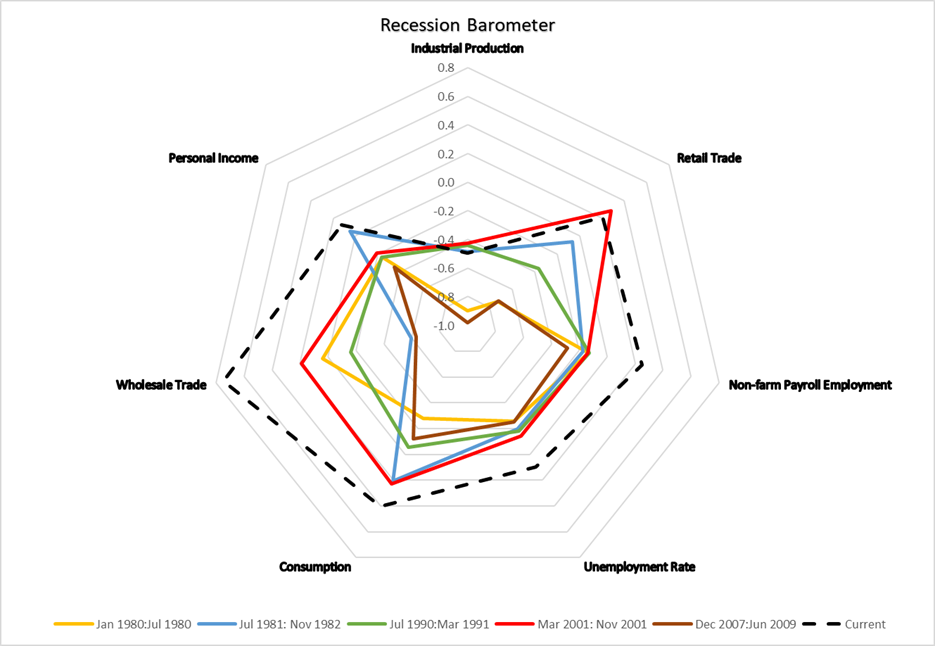

The updated radar plot compares the current NBER indicator values with the average monthly growth for each recession from 1980 through the Great Recession. The pandemic recession was excluded due to its peculiar nature. For current values, we used an average of Dec 2022 and Jan 2023 to smooth out potential problems with seasonal adjustments. There is still very little indication that the economy is in a recession. Industrial production has been weak and real income growth is slowing, but the other indicators remain strong.

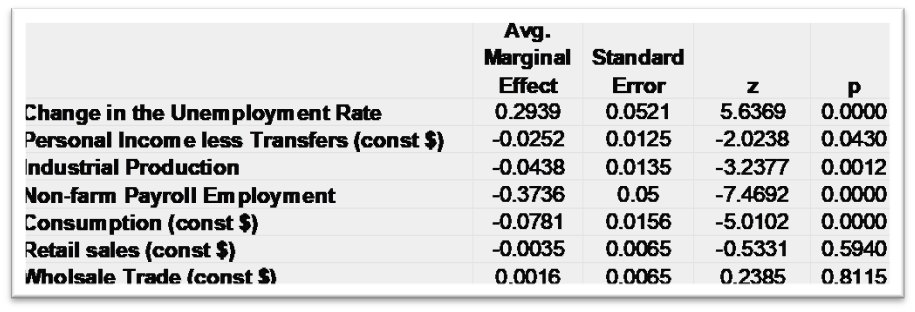

As we highlighted in our previous piece, to get a sense of the relative importance of the different factors we estimated a logistic regression using the 7 series in Figure 1 as explanatory variables, and an indicator variable (1 for recession, 0 otherwise) as the dependent variable. We used data from Jan. 1959 to present, so there are 9 recessions. The average marginal effects are in the following table. All of the variables except retail sales and wholesale trade are statistically significant. The labor variables have the greatest impact. An increase in the unemployment rate by 1.0% will increase the probability of a recession by 29%. A 2% decrease in non-farm payroll employment (about 3mln jobs lost in a year these days) will increase the probability of a recession by 74%.

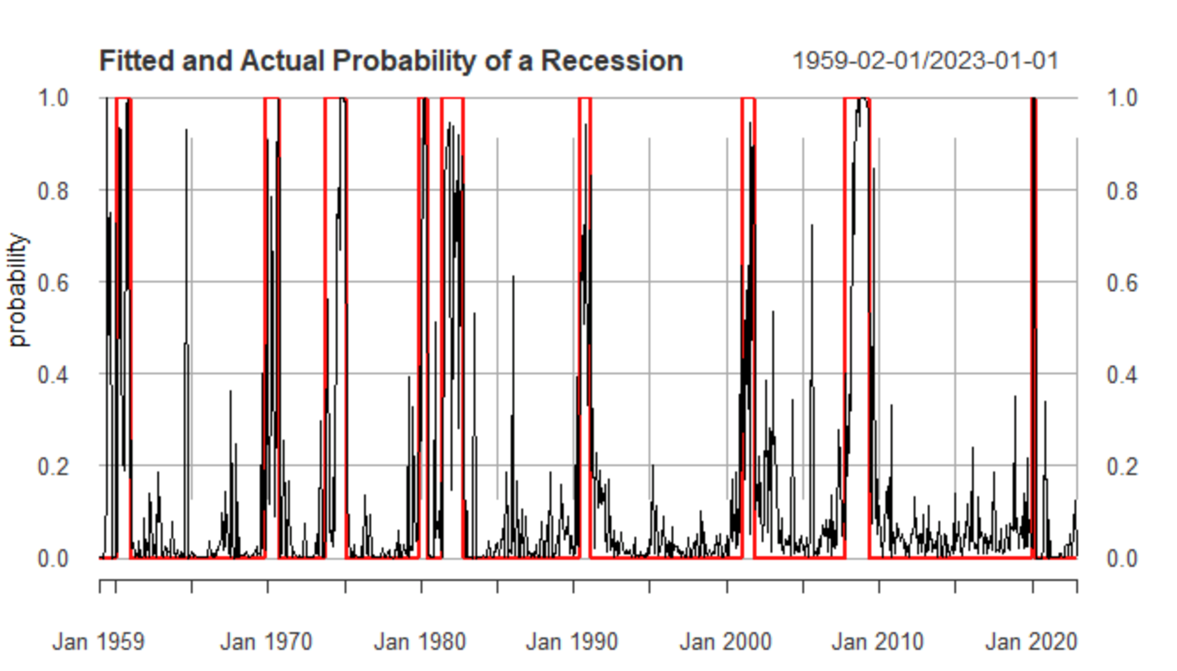

Below we update this estimate of the probability of a recession using data from Jan. 1959 to Jan. 2023. According to this model, the probability that the economy is in a recession is low and even lower than it was in November.

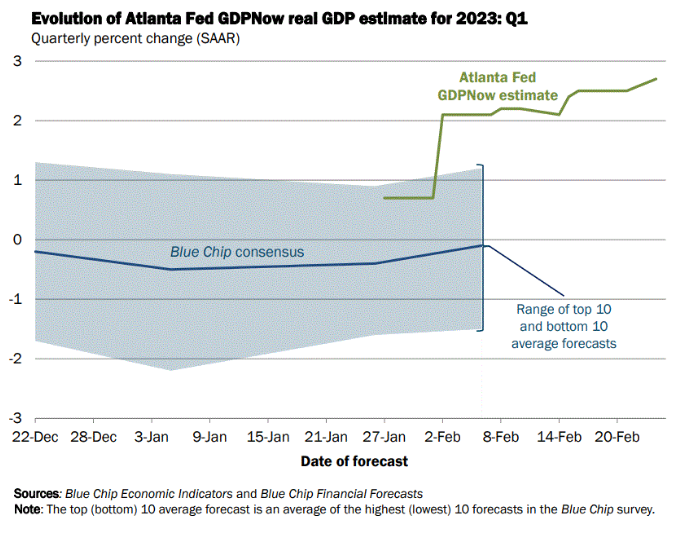

This shouldn’t come as all that much of a surprise given where these growth stats are coming out. Our model is directionally consistent with the Atlanta Fed GDPNow estimate of +2.7% for Q1 real GDP growth (see Figure 3). Interestingly, the Blue Chip consensus ranges from -1.5% to +1.1%, with an average slightly below zero. The Blue Chip projections place much more weight on expectations than the actual data.

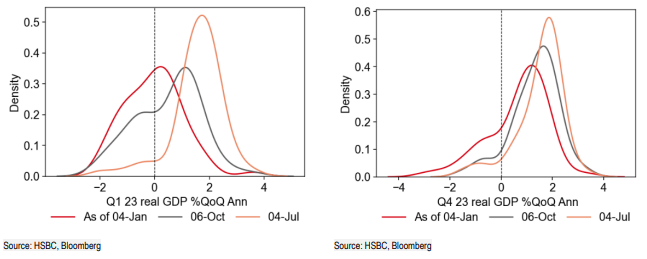

Entering this year, the majority of market prognosticators believed the economy was in recession. The chart on the left highlights how the distribution of Real GDP estimates for 1Q23 were centered around zero with the vast majority of the views below zero and essentially none predicting 2%. As our model highlighted a couple months ago, the data did not align with that view and continues to do so today.

Real GDP Expectations By Quarter, As of January 2023

This has important implications for investors as this adjustment to the likelihood of stronger growth for longer gets repriced through the financial markets. For bond market investors, this is particularly difficult as expectations of future cuts come out of the pricing. But it’s no clear bullish sign for the stock market. Stronger growth will require tighter monetary policy and a harder eventual landing to ease inflation pressure. As we highlighted 6 weeks ago, these dynamics continue to align to be particularly difficult for the 60/40 portfolio moving forward.

For informational and educational purposes only and should not be construed as investment advice. The historical analysis discussed herein has been selected solely to provide information on the development of the research and investment process and style of Unlimited. The historical analysis should not be construed as an indicator of the future performance of any investment vehicle that Unlimited manages. No investment strategy or risk management technique can guarantee return or eliminate risk in any market environment. No Representation is being made that any investment will or is likely to achieve profits or losses similar to those shown herein.